The Big Three: Equifax, Experian, and TransUnion

The three major credit bureaus — Equifax, Experian, and TransUnion — maintain credit reports on almost all Americans with credit history. These reports include payment history, credit accounts, inquiries, and negative items. Lenders use these reports to decide whether to approve you and what interest rate to charge. Inaccurate information directly impacts your ability to borrow.

Dispute errors in writing, not by phone. Send certified mail with return receipt to prove you contacted the bureau. Include copies (not originals) of documentation supporting your dispute. The bureau must investigate within 30 days and report back. If they can't verify the accuracy of the error, they're required to remove it or correct it.

Some errors are creditor reporting mistakes, not bureau mistakes. If a creditor reported an account closed when it's open, or reported a late payment that didn't happen, dispute it with both the creditor and the bureau. The creditor must update their reporting within 15 days; the bureau must update within 30 days. Get both in writing.

Your credit report is free to check once yearly from AnnualCreditReport.com. Credit monitoring services cost extra ($10-15 monthly) but monitor your report automatically for changes and alert you to new accounts or inquiries. If you've had fraud or are a financial nervous person, it might be worth the cost. But the free annual report is sufficient if you check it carefully yearly.

How Creditors Report Information

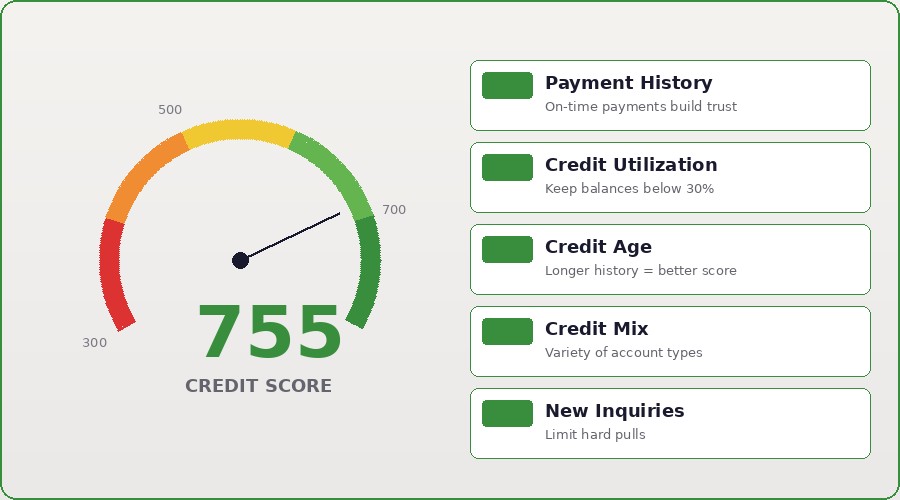

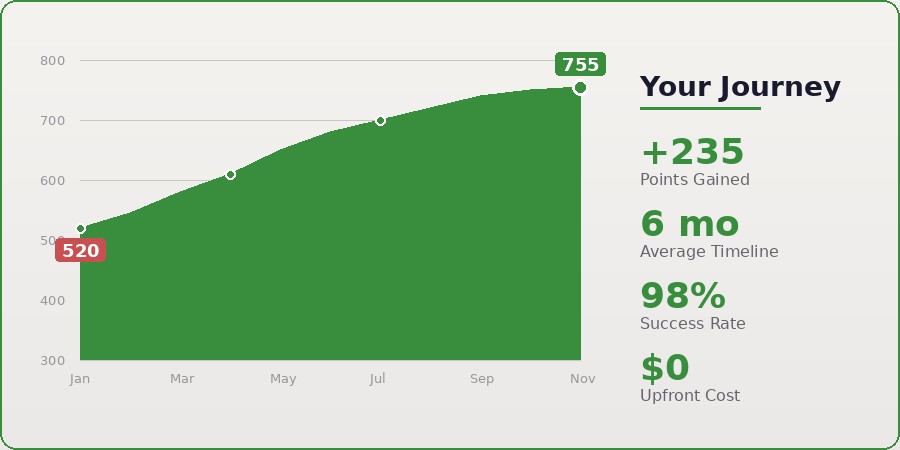

Good credit repair isn't a single move — it's a comprehensive approach combining multiple strategies simultaneously. Check your reports for errors (dispute inaccuracies), reduce balances (payment history and utilization), become an authorized user on positive accounts (mix and age), stay current on all new payments (the most important factor), and wait for negative items to age (time heals credit wounds).

The timeline for visible results is 3-6 months if you're aggressive. If you dispute errors, you might see those removed in 30-90 days. If you pay down balances, your score improves within 1-2 billing cycles. If you get added as an authorized user, that score boost happens instantly. The compounding effect of multiple moves gives you 50-100 point improvements relatively quickly.

Realistic expectations: you can't remove accurate negative information, but you can dispute inaccurate items. You can't make old items disappear (but their impact fades over time). You can build a positive credit file starting today. Recovery from 450 credit to 700 credit typically takes 18-36 months with consistent action. It's not overnight, but it's absolutely achievable.

Work with credit professionals if DIY isn't moving the needle. Good credit repair companies combine dispute expertise, creditor negotiation skills, and strategic guidance. Legitimate companies charge ongoing fees (not upfront), give honest timelines, and focus on disputing inaccuracies and negotiating with creditors. The cost is worth it if it saves you months of effort and adds years to your credit recovery timeline.

Understanding Your Credit Report Sections

About 1 in 5 credit reports contain errors according to FTC studies — that's 40+ million Americans with wrong information on their credit reports. Errors range from incorrect balances to accounts that aren't yours to closed accounts listed as open. Your credit score is only as accurate as the information on your report, so checking it annually is non-negotiable.

Get free credit reports yearly from AnnualCreditReport.com (the only government-authorized free source). Check all three bureaus separately — Equifax, Experian, and TransUnion — because information varies. Look for incorrect accounts, wrong balances, inaccurate payment history, and accounts listed twice. Take detailed notes on any errors you find.

Once you spot an error, file a dispute in writing within 30 days of receiving your report. Send copies of documentation proving the error (account statements, payment receipts, proof of paid-off accounts). The bureau has 30 days to investigate and respond. Most bureaus process disputes faster now (10-15 days), but they're legally allowed 30 days.

Equifax, Experian, and TransUnion sometimes have different information because not all creditors report to all three bureaus. Your credit score with Equifax might be 680, with Experian 710, with TransUnion 695. This is why checking all three annually is important. If one bureau has an error the others don't, fix that bureau specifically.

When Credit Bureaus Get It Wrong

The three major credit bureaus — Equifax, Experian, and TransUnion — maintain credit reports on almost all Americans with credit history. These reports include payment history, credit accounts, inquiries, and negative items. Lenders use these reports to decide whether to approve you and what interest rate to charge. Inaccurate information directly impacts your ability to borrow.

Dispute errors in writing, not by phone. Send certified mail with return receipt to prove you contacted the bureau. Include copies (not originals) of documentation supporting your dispute. The bureau must investigate within 30 days and report back. If they can't verify the accuracy of the error, they're required to remove it or correct it.

Some errors are creditor reporting mistakes, not bureau mistakes. If a creditor reported an account closed when it's open, or reported a late payment that didn't happen, dispute it with both the creditor and the bureau. The creditor must update their reporting within 15 days; the bureau must update within 30 days. Get both in writing.

Your credit report is free to check once yearly from AnnualCreditReport.com. Credit monitoring services cost extra ($10-15 monthly) but monitor your report automatically for changes and alert you to new accounts or inquiries. If you've had fraud or are a financial nervous person, it might be worth the cost. But the free annual report is sufficient if you check it carefully yearly.

Fighting Bureau Errors with 755CreditScore

The three major credit bureaus — Equifax, Experian, and TransUnion — maintain credit reports on almost all Americans with credit history. These reports include payment history, credit accounts, inquiries, and negative items. Lenders use these reports to decide whether to approve you and what interest rate to charge. Inaccurate information directly impacts your ability to borrow.

Dispute errors in writing, not by phone. Send certified mail with return receipt to prove you contacted the bureau. Include copies (not originals) of documentation supporting your dispute. The bureau must investigate within 30 days and report back. If they can't verify the accuracy of the error, they're required to remove it or correct it.

Some errors are creditor reporting mistakes, not bureau mistakes. If a creditor reported an account closed when it's open, or reported a late payment that didn't happen, dispute it with both the creditor and the bureau. The creditor must update their reporting within 15 days; the bureau must update within 30 days. Get both in writing.

Your credit report is free to check once yearly from AnnualCreditReport.com. Credit monitoring services cost extra ($10-15 monthly) but monitor your report automatically for changes and alert you to new accounts or inquiries. If you've had fraud or are a financial nervous person, it might be worth the cost. But the free annual report is sufficient if you check it carefully yearly.