When Do You Need a Credit Repair Lawyer?

Federal credit laws are stronger than most people realize. The FCRA allows you to dispute inaccurate information at no cost. The FDCPA makes debt collection a minefield for collectors if they don't follow procedures exactly. The CROA cracks down on credit repair scams. Knowing your rights turns the tables from creditors being in power to you having real protection.

The FCRA requires credit bureaus to provide free reports annually, investigate disputes within 30 days, and remove inaccurate information. If they fail these requirements, you can sue. Max damage is $1,000 per violation plus attorney fees. Hundreds of FCRA lawsuits are filed annually by people with legitimate claims. If a bureau ignores your dispute or removes your name wrong, you have legal recourse.

The FDCPA gives collectors no wiggle room. They can't call before 8 AM or after 9 PM (even weekends). They can't contact your workplace without permission. They can't contact you if you've sent a written request to stop (cease and desist letter). They can't harass, threaten, or make false statements about the debt. Violating these rules means statutory damages of $1,000 per violation plus your actual damages.

The CROA makes it illegal for credit repair companies to charge upfront before delivering results, to misrepresent what they can do, or to prevent you from contacting the credit bureaus directly. They must give you a written contract, let you cancel within 3 days, and operate with full transparency. Violating CROA is a federal crime. If a company breaks these rules, sue them.

Credit Counseling vs Legal Representation

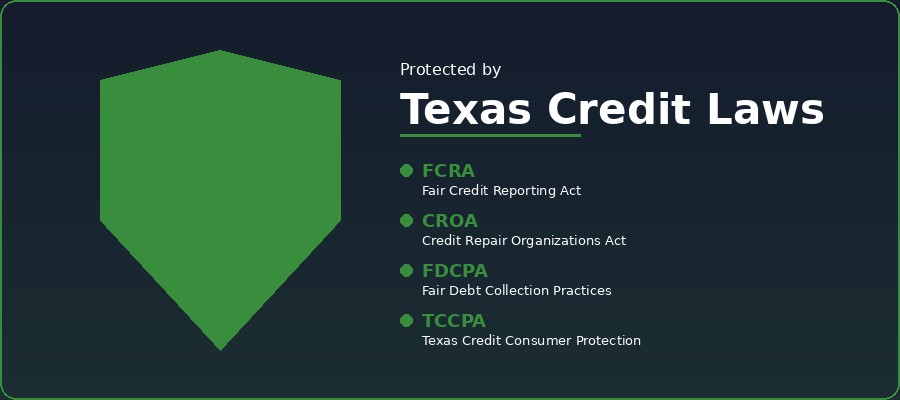

The Fair Credit Reporting Act (FCRA) protects you from inaccurate credit reports and unauthorized inquiries. The Fair Debt Collection Practices Act (FDCPA) protects you from collector harassment. The Credit Repair Organizations Act (CROA) protects you from credit repair scams. Texas Credit Consumer Protection Act (TCSOA) adds state-level protections. Together, these laws give you serious ammunition against predatory practices.

Red flags of credit repair scams: upfront fees before any work (illegal), claims they can remove accurate negative information (impossible), claims of special 'secret methods' to remove accurate items, guaranteed score improvements, and pressure to sign quickly. Legitimate credit professionals charge reasonable ongoing fees, give you honest timelines, and only promise to dispute inaccurate items.

The CROA has a 3-day cancellation right: you can cancel with any credit repair company within 3 days and get a full refund. The company must provide you a written cancellation form, a description of your rights, and a copy of any contract. If they don't, they're violating federal law and you have grounds to sue them.

The FDCPA explicitly prohibits collector harassment: no calls before 8 AM or after 9 PM, no contact with your employer, no threats of arrest or jail time, no unlimited phone calls, no false representations of authority. Validate the debt within 30 days and collectors must prove they own it. Sue for damages if they violate these rules — many lawyers take FDCPA cases on contingency.

Consumer Protection Laws That Protect You

Federal credit laws are stronger than most people realize. The FCRA allows you to dispute inaccurate information at no cost. The FDCPA makes debt collection a minefield for collectors if they don't follow procedures exactly. The CROA cracks down on credit repair scams. Knowing your rights turns the tables from creditors being in power to you having real protection.

The FCRA requires credit bureaus to provide free reports annually, investigate disputes within 30 days, and remove inaccurate information. If they fail these requirements, you can sue. Max damage is $1,000 per violation plus attorney fees. Hundreds of FCRA lawsuits are filed annually by people with legitimate claims. If a bureau ignores your dispute or removes your name wrong, you have legal recourse.

The FDCPA gives collectors no wiggle room. They can't call before 8 AM or after 9 PM (even weekends). They can't contact your workplace without permission. They can't contact you if you've sent a written request to stop (cease and desist letter). They can't harass, threaten, or make false statements about the debt. Violating these rules means statutory damages of $1,000 per violation plus your actual damages.

The CROA makes it illegal for credit repair companies to charge upfront before delivering results, to misrepresent what they can do, or to prevent you from contacting the credit bureaus directly. They must give you a written contract, let you cancel within 3 days, and operate with full transparency. Violating CROA is a federal crime. If a company breaks these rules, sue them.

How to Choose the Right Help

Start your DIY credit repair by checking your reports for accuracy. Getting your free annual report is step zero. Pulling your Equifax, Experian, and TransUnion reports separately (they're usually different) gives you the full picture of what's damaging your score. Review line by line: account names, balances, payment status, account ages.

Certified mail is non-negotiable for disputes. Regular mail gets lost; certified mail with return receipt creates proof you contacted the bureau with a dispute request. The return receipt shows they received it; the certified tracking shows the date. This documentation protects you if the bureau claims they never got your dispute.

Dispute inaccurate information aggressively. If a debt is listed as 'still owed' when you paid it off, dispute it. If a late payment shows from 2019 but you were never late in 2019, dispute it. The burden is on the creditor to prove accuracy, not on you to prove inaccuracy. Many errors get removed simply because creditors can't verify the accuracy.

If DIY disputes fail after 3-4 attempts, consider hiring a credit professional. The FTC and state law give you some protection: legitimate credit repair companies charge reasonable fees, deliver realistic results, and don't claim they can remove accurate negative information. Scams promise removal of accurate information or charge upfront before delivering results — avoid those entirely.

Start with a Free Credit Consultation

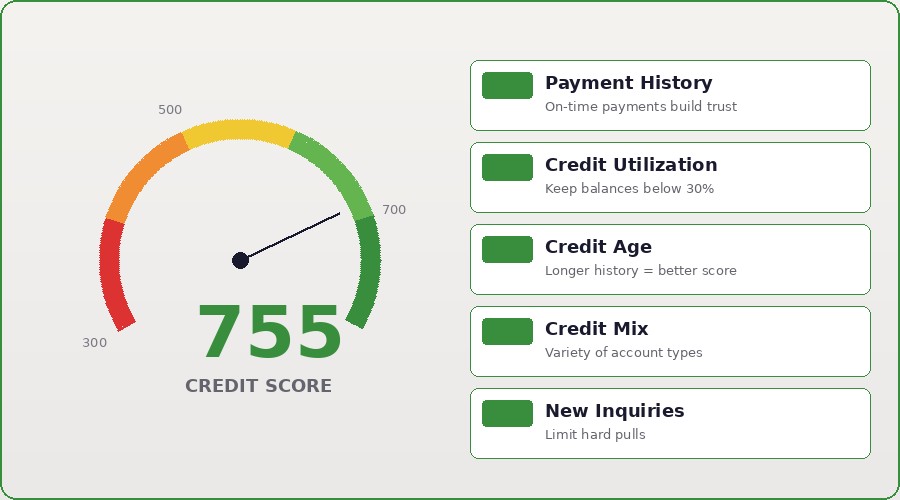

Credit repair is fundamentally about managing three factors: accuracy of reports, payment behavior going forward, and aging of negative items. You can't change history, but you can correct inaccuracies, prove you're financially responsible now, and let time fade old damage. Most people dramatically underestimate what's possible because they think accurate negative information is permanent (it fades in power over time).

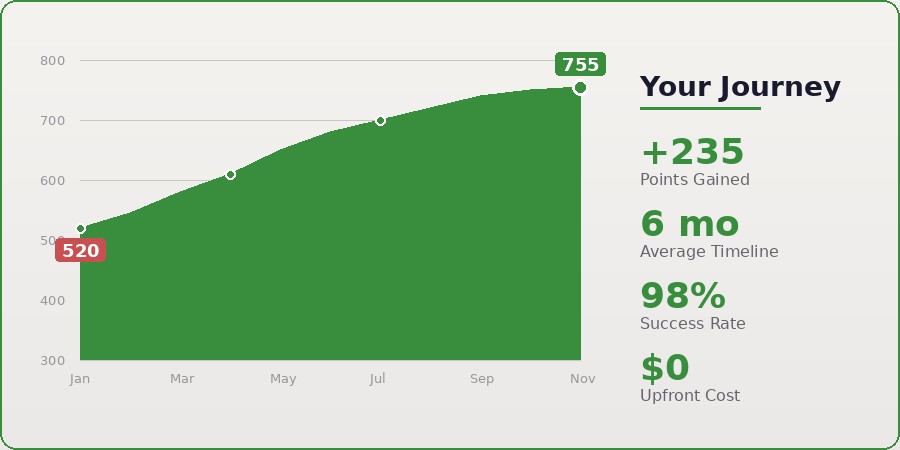

Start by checking your reports (free at AnnualCreditReport.com), identifying errors, and disputing inaccuracies in writing. While disputes process, focus on new credit behavior: pay every bill on time, reduce existing balances, avoid new hard inquiries. This dual approach of fixing reports while building positive history compounds over months.

Add yourself to positive accounts as an authorized user if possible. Family or friends with excellent credit and high limits can add you to their account. Their payment history and age show up on your report, boosting your score instantly by 50-100 points in many cases. There are no downsides if the primary account holder has perfect payment history and low utilization.

Becoming current on all accounts is critical. Stop the bleeding first. If you have delinquent accounts, get current immediately. One month of current payments doesn't erase the delinquency history, but it stops the daily credit score damage. After 3-6 months of current payments on previously delinquent accounts, you'll see significant score improvements.